Profitability of Broiler Chicken Business in Kudus Regency, Central Java, Indonesia

Research Article

Profitability of Broiler Chicken Business in Kudus Regency, Central Java, Indonesia

Siswanto Imam Santoso*, Agus Setiadi, Maulina Syafa’ati Ningrum

Agribusiness, Faculty of Animal and Agricultural Sciences, Universitas Diponegoro, Semarang, Indonesia.

Abstract | This research aims to analyze the profitability of the broiler farming business in partnership with Ciomas Adisatwa Ltd in Kaliwungu District, Kudus Regency. This research uses a survey method. The sampling method in this study was total sampling or census with a total of 6 farmers. The sample was divided into two levels: strata I 1-30,000 broilers and strata II > 30,000 broilers chicken. The data analysis method used was descriptive statistical analysis. Data were analyzed using the formula for production costs, total revenue, and profitability, BEP, payback period (PP), and R/C ratio. The statistical analysis used was the normality test and the one-sample t-test. The results of this study show that the broiler farm business in Kaliwungu District, Kudus Regency is profitable, with strata I being more profitable than strata II. There is no difference in the results of the one-sample t-test at the stratum II level, and for stratum I, there is a significant difference between the profitability of the broiler farm and BRI Bank deposits.

Keywords | Broilerchicken, Kudus Regency, Farmer, Profitability, Feasible .

Received | June 22, 2023; Accepted | July 20, 2023; Published | December 01, 2023

*Correspondence | Siswanto Imam Santoso, Agribusiness, Faculty of Animal and Agricultural Sciences, Universitas Diponegoro, Semarang, Indonesia; Email: siswantoimamsantoso@lecturer.undip.ac.id

Citation | Santoso SI, Setiadi A, Ningrum MS (2023). Profitability of broiler chicken business in kudus regency, central java, Indonesia. Adv. Anim. Vet. Sci. 11(12): 2075-2081.

DOI | http://dx.doi.org/10.17582/journal.aavs/2023/11.12.2075.2081

ISSN (Online) | 2307-8316

Copyright: 2023 by the authors. Licensee ResearchersLinks Ltd, England, UK.

This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

INTRODUCTION

Farmer is an example of a business that can support the economy of rural communities. The problems faced in developing smallholder livestock businesses are the need for more business capital for breeders and marketing aspects of livestock products. The solution to the problem of increasing livestock business income is to run a partnership pattern. The company engaged in poultry partnerships is Ciomas Adisatwa, a Japfa Comfeed Indonesia Ltd subsidiary. Ciomas Adisatwa manages broiler partnerships with community breeders. The broiler business is quite perspective because people’s appetite for chicken taste is very high in all circles. The profit value obtained is relatively high if managed effectively and efficiently. Based on data from the Central Bureau of Statistics, in 2018, the highest broiler production in Central Java was Semarang City, which was 19,327 tons. However, in 2019 the highest broiler production was taken over by Demak Regency, which was 20,416.6 tons. Profitability is very important to develop agriculture commodity in Indonesia (Purbajanti et al., 2016). Setiadi et al. (2022) stated that broiler chicken business in Indonesia is profitable. Further they (2022) stated that the profitability obtained from broiler chicken business almost 30% per year in Indonesia.

Based on data from the Central Statistics Agency, the population of broiler chickens in Kudus Regency in 2019 was 10,155,200, and in 2020 it increased to 18,440,400. This increase in the broiler population shows that there has been an increase in business from 2019 to 2020. Kudus Regency has also experienced an increase in meat production, initially in 2018, namely 8,530.37 tons to 13,277.09 tons. Kudus Regency is the highest broiler meat producer at the Pati Residence level, which can produce 62.83% of the total broiler meat production in the Pati Residence. Broiler chicken farming in Kaliwungu District produces 26.88% of the entire broiler chicken population produced by Ciomas Adisatwa Ltd partnership in Kudus Regency.

An increase in meat production can be a sign that there has been an increase in livestock farming. Increasing the livestock business will undoubtedly make many people interested in taking part in opening a livestock business. Broiler chicken businesses in Kaliwungu District and Kudus Regency have different production capacities. It is possible for farmers who have a large livestock population to obtain a higher level of income and profitability compared to those with a small livestock population. A large number of livestock results in high operational costs, so a study is needed to determine the profitability level achieved from different livestock ownership scales.

This study aimed to determine the level of profitability obtained by broiler breeders following a partnership pattern with different livestock ownership scales. Another advantage of this research is that if there is an entrepreneur who intends to open a broiler farm in Kaliwungu District, Kudus Regency, then they already knows the most profitable livestock population, making it easier to estimate the financial and return on capital of the broiler farm that will be run.

RESEARCH METHODOLOGY

The method used in this research is a survey method. This research was conducted from 12 October 2022 to 5 November 2022 with a research location in Kaliwungu District, Kudus Regency. The selection of the location was made deliberately or purposively. The sampling used in this study was non-probability sampling, and the sampling method used was total sampling. The samples to be taken are all partner farmers of Ciomas Adisatwa Ltd. in Kaliwungu District, Kudus Regency.

The samples obtained were divided into two levels: strata I <1-30,000 broilers and strata II >30,000 broilers. The study used primary data from unstructured interviews with broiler breeders partnered by Ciomas Adisatwa Ltd in Kaliwungu District, Kudus Regency, and secondary data in the form of farmer rearing results recapitulation and the number of partner breeders in the Kaliwungu District, Kudus Regency. Obtained from PT Ciomas Adisatwa. The data obtained were analyzed through the following stages:

Determine production costs (total cost) using the following formula.

TC=TFC+TVC

Explanation:

TC = Total cost (total cost)

TFC = Total fixed costs

TVC= Total variable cost

Determine acceptance by using the formula:

TR=P x Q

Explanation:

TR = total revenue

P=Price (price)

Q=Quantity (amount)

Determining BEP with the formula from Hastuti et al. (2018):

BEP unit= (Total Production Cost (IDR))/(Chicken Price (IDR⁄Kg))

BEP price = (Total Production Cost (IDR))/(Total Production (Kg))

Determine profitability ratios:

Profitability= (Net income)/(Total cost) x 100%

The results of the profitability ratio are compared to Bank BRI’s deposit interest rate in October 2021, which is 2.85% for a 1-year tenor. If profitability > the prevailing bank deposit rate, broiler farming is profitable. If profitability < the prevailing bank deposit rate, broiler farming is unprofitable. This comparison was tested by One sample t-test using the SPSS application version 26. The difference between the value of profitability and current interest rates is known by using One sample t-test.

H0: µ1 = interest rate, meaning there is no difference between profitability and prevailing interest rates.

H0: µ1 ≠ interest rate, meaning that there is a difference between profitability and prevailing interest rates. The test criteria used, namely if:

If the significance value > 0.05, H0 is accepted, and H1 is rejected.

Significance value ≤ 0.05 then, H0 is rejected and H1 is accepted

The requirement for the one-sample t-test is that the data must be normally distributed. The normality test results on SPSS 26 used in this study are based on the Shapiro-Wilk analysis.

Hypothesis:

H0: data on profitability values are normally distributed

H1: profitability value data is not normally distributed

The test criteria used, namely if:

If the significance value > 0.05, H0 is accepted, and H1 is rejected.

Significance value ≤ 0.05 then, H0 is rejected and H1 is accepted

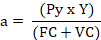

The R/C ratio was computed using the formula :

Explanation:

R = Revenue

C = Cost

Py = Price of Output

Y = Output

FC = fixed cost

VC = Variable cost

a = R/C ratio

Decision-based on Payman’s decision (1993):

If the value of the R/C ratio < 1, broiler chicken farming is declared unfit for development.

If the value of the R/C ratio = 1, broiler chicken farming is declared unfit for development.

If the value of the R/C ratio > 1, broiler chicken farming is declared feasible to be developed.

The payback period is used to analyze financial feasibility based on how much capital can be returned. The payback period formula is as follows:

Payback period = (initial investment)/(net cash) x 1 year

PP assessment criteria:

If PP < Minimum payback is the same as the age of the broiler farm, it means that the broiler farm in Kaliwungu District, Kudus Regency is feasible.

If PP ≥ minimum payback is the same as the age of the broiler farm, it means that the broiler farm in Kaliwungu District, Kudus Regency, is not feasible.

RESULTS AND DISCUSSION

Research Site

Kaliwungu is a sub-district in Kudus Regency, Central Java Province, Indonesia. Kaliwungu is a sub-district located in the western part of the Kudus Regency. To the east, it is bordered by Kota District; on the north, it is bordered by Gebog District; on the west, it is bordered by Nalumsari District, Jepara Regency. To the south, it is bordered by Jati District and Karanganyar District, Demak Regency. Kaliwungu District is the largest sub-district in Kudus Regency.

Based on data from the Kudus Regency Agriculture Service in 2020, it is known that 41 dairy cows, 534 cows, 788 buffaloes, nine horses, 2,875 goats, and 2,760 sheep. The number of poultry in Kaliwungu District in 2020 totaled 1,714,870, consisting of 4574 ducks, 1,684,400 broiler chickens, and 25,896 native chickens. The highest number of ducks was in Garung Kidul Village, with 4,399 heads; the highest population of Broiler chickens was in Prambatan Kidul Village, with 700,000 tails, and the highest native chicken population in Kaliwungu Village, with 2,217 ducks.

Respondents Characteristics

Respondents in this study consisted of 5 breeders and six cages. The selection of respondents was carried out by taking all partner farmers of PT Ciomas Adisatwa in Kaliwungu District, Kudus Regency, which are known based on partner data from the unit office of PT Ciomas Adisatwa, Kudus branch. 100% of breeders in this study were still of productive age, namely in the range of 24-37 years. The number of the population owned by breeders will affect their level of income, the highest population in this study was 52,000 heads, and the lowest population in this study was 13,000 heads.

Revenue

Farmers’ revenue in Kaliwungu District, Kudus Regency, was obtained from chicken sales, market price subsidies, efficiency differences, market price subsidies, and broiler chicken rearing incentive. The average value of broiler breeders’ acceptance in Kaliwungu District, Kudus Regency, at each stratum can be seen in Table 1.

Based on the data in Table 1, it is known that the average income for farmers in strata I was IDR. 585,560,902 and in strata II, which was IDR. 1,556,632,930. Income from strata II is greater than income from farmers from strata I. The largest income from broiler chicken farming in Kaliwungu District, Kudus Regency at strata I and strata II comes from the sale of chickens. The number of chicken sales in strata I IDR. Rp. 585,560,902 with a percentage of 98.362%, while in strata II, namely IDR. 1,537,069,625. with a percentage of 98.743%. The percentage value of chicken sales in strata II is higher than that of strata I. This is because the population of strata II is larger than strata I, so more chickens are sold. Utomo et al. (2015) state that a reared large broiler population affects the high sales of chickens, performance subsidies, and market price subsidies received by plasma.

Cost Production

Table 2 shows that the fixed costs of a broiler farm in Kaliwungu District, Kudus Regency include costs for depreciation of cages and equipment and PBB costs. Variable costs incurred by breeders in Kaliwungu District include the cost of purchasing DOC, feed, husks, electricity, chemical drugs and vaccines, gas, salaries of crew members, money for the cost of lowering feed, costs for harvesting labor, and payments for disposal of husks. This is supported by Simanjuntak’s statement (2018), which states that fixed costs in the livestock business are in the form of land and cage rental costs. Variable costs are costs whose size is affected by the farm’s production, such as seeds (DOC), feed, medicines and vaccines, electricity, and labor expressed in rupiah (IDR).

Table 2 shows that the fixed costs and variable costs in the broiler farming business in Kaliwungu District, Kudus Regency are higher variable costs for each stratum. The total fixed cost of strata I was IDR. 2,887,306.2 with a percentage of 0.543% and at strata II fixed costs, namely IDR. 9,173,318 with a percentage of 0.637%. The most enormous fixed costs incurred in a production process in strata I and strata II are found in the depreciation of cages and equipment, where the value in strata I was IDR. 2,864,033.5 with a percentage of 0.539% and a grade II value of IDR. 9,124,448, which is 0.634%.

The total strata I variable cost was IDR. 528,695,094 with a percentage of 99.457% and in strata II, namely IDR. 1,429,851,048 with a percentage of 99.363%. The highest variable costs incurred in a production process at strata I and strata II are found in the purchase of feed, which has a value of about 70%. The value in strata I was IDR. 385,443,550 with a percentage of 72.509% and a grade II value of IDR. 1,027,705,525, which is 71.417%. This follows the opinion of Saputra et al. (2014), which states that farmers desire to create optimal output with minimal feed costs because feed costs contribute the most, around 60% -70%.

Profitability Analysis

The value of profitability is a value that is used to measure whether a broiler farm business in Kaliwungu District, Kudus Regency is profitable. This statement is supported by Prasetyo et al. (2018), which state that the profitability analysis aims to determine the profit that business actors get by subtracting total revenue from the total expenditure. The profitability value obtained by breeders at the strata I level obtains a profitability value of IDR. 53,978,502 with a percentage of 9.218% and breeders at the strata II level of IDR. 117,608,564, with a percentage of 7.555% .

The profitability percentage between strata I and II is known to be higher for strata I. This is because the costs incurred in strata II are greater than those incurred by strata I, and their use could be more efficient. The broiler population also affects profitability because large populations cause delays in feeding and cause high chicken densities that will affect chicken development. This follows the statement of Rukmini et al. (2019), which states that high livestock density can result in lower chicken weight gain. Another factor that results in a low profitability value is that the average IP value in strata II is smaller than in strata I. This statement is supported by Paly (2016), which states that the higher the Index Performance (IP) value, the more successful the chicken farm will be. The IP value for each stratum on broiler farms in Kaliwungu District is considered good because the value is greater than the standard IP value. This statement is supported by a statement (Santoso et al., 2018) stating that the IP standard for broiler chickens with good farm management is 300; if the IP value is higher, it shows better farm management. IP of Strata I was 411, while in strata II was 384.

BEP Analysis

Based on the data in Table 3, it is known that the unit BEP value and BEP price for broiler chicken farms in Kaliwungu District, Kudus Regency, in strata I and strata II have a higher production value than the BEP value. The breakeven point (BEP) on broiler farms in the Kaliwungu sub-district is when the business experiences neither profit nor loss. This statement is supported by the opinion of Hayati et al. (2019), which states that BEP is a condition in which a business neither gains nor suffers losses. There are 2 BEP values for broiler chicken business: unit BEP and price BEP.

Broiler chicken farms in strata I will experience a breakeven point if they sell 20,509 kg of reared chickens for IDR. 18,509, but the farmer could sell 28,721 kg of reared chickens for IDR. 20,059. Broiler chicken farms in strata II will experience a breakeven point if they sell 71,795.77 kg of reared chickens for IDR. 18,757, but breeders could sell 76,718.83 Kg of reared chickens for IDR. 20,043. The production value is greater than the BEP value indicating that broiler chicken farms in Kaliwungu District are experiencing profits. This follows the opinion of Zentiko et al. (2015), which states that if the final sale of a business only reaches the unit BEP and rupiah BEP points, the business is at a breakeven point. In contrast, the business will receive income if it sells maintenance results above the BEP. Vice versa, will lose money if sales are below the BEP value.

The BEP value for broiler chicken farms in the Kaliwungu sub-district, Kudus district, is higher than the results of research from Setiadi et al. (2021), which results in a BEP value for the price of closed house cages, namely IDR. 14,764, and the results of research from Suasta et al. (2019), obtained a price BEP value for a closed-house cage system. IDR 16,032. This is due to the inefficiency of operational costs when raising chickens, which causes expenses to swell, and the higher price of DOC, and IDR. 7,750-, whereas in Setiadi et al. (2021), the DOC price is IDR. 5,450 and in Suasta et al. (2019), the DOC price is IDR. 6.190-. A considerable DOC value also causes production costs to be higher, causing a higher BEP value. This is supported by the statement of Maulana (2017), which states that broiler farming businesses cannot stem the high production prices resulting from relatively more expensive DOC and feed prices.

Table 1: Revenue of Broiler Business

|

No |

Revenue |

Strata I | Strata II | ||||||||

| Number | Percentage | Number | Percentage | ||||||||

| . . IDR . . | . . % . . | . . IDR . . | . . % . . | ||||||||

| Broiler chicken sold | 575,969,266 | 98.36 | 1,537,069,625 | 98.74 | |||||||

| difference in efficiency |

6,849,915 |

1.17 | 17,653,696 | 1.13 | |||||||

| Market price subsidize | 2,741,722 | 0.47 | 309,608 | 0,02 | |||||||

| Rearing incentive | 0 | 0 | 1,600,000 | 0,10 | |||||||

| Revenue | 585,560,902 | 100 |

1,556,632,930 |

100 | |||||||

Sources: Primary data 2022

Table 2: The production cost of broiler chicken business

|

No |

Production Cost |

Strata I | Strata II | |||||||

| Number | Percentage | Number | Percentage | |||||||

| . . IDR . . | . . % . . | . . IDR . . | . . % . . | |||||||

| 1 | Fix Cost | |||||||||

| Cage and facility depreciation | 2.864.033,5 | 0.539 | 9,124,448 | 0.634 | ||||||

| Property tax | 23.272,6 | 0.004 | 48,871 | 0.003 | ||||||

| Fix cost total | 2.887.306,2 | 0.543 | 9,173,318 | 0.637 | ||||||

| 2 | Variable cost | |||||||||

| DOC | 114,500,500 | 21.540 |

317,004,750 |

22.029 | ||||||

| Feed | 385,443,550 | 72.509 | 1.027,705,525 | 71.417 | ||||||

| Gas | 4,775,000 |

0.898 |

11,870,000 | 0.825 | ||||||

| Rice husk | 2,610,000 |

0.491 |

7,425,000 | 0.516 | ||||||

| Electricity | 4,802,641 | 0.903 | 19,077,970 | 1.326 | ||||||

| Drug and Vitamin | 2,864,977 | 0.539 | 8,597,896 | 0.597 | ||||||

| Worker salary |

8,868,350 |

1,668 | 23,561,665 | 1.637 | ||||||

| Worker Food | 1,250,000 | 0.235 | 3,250,000 | 0.226 | ||||||

| Feed down wages | 513,100 | 0.097 | 1,636,465 | 0.114 | ||||||

| Harvested wage | 2,116,976 | 0.398 | 4,059,277 | 0.282 | ||||||

| Rice husk disposal | 800,000 | 0.150 | 2,812,500 | 0.195 | ||||||

| Gazoline | 150,000 |

0.028 |

2,850,000 | 0.198 | ||||||

| Variable cost total | 528,695,094 | 99.457 | 1,429,851,048 | 99.363 | ||||||

| Production cost total | 531,582,400 | 100 | 1,439,024,367 | 100 | ||||||

Sources: Primary data 2022

Table 3: Break Even Point (BEP) of broiler chicken business.

|

No |

Item |

Strata I | Strata II | ||

| Production Total | Broiler Price | Production Total | Broiler Price | ||

| . . Kg . . | . . IDR . . | . . Kg . . | .. . IDR . . | ||

| Production | 28,721 | 20,059 |

76,718.83 |

20,043 | |

| BEP | 26,501 | 18,509 | 71,795.77 |

18,757 |

|

Sources: Primary data 2022

Analysis R/C ratio (Revenue cost ratio)

R/C ratio analysis is used to determine whether a livestock business is profitable. Usually, R/C ratio analysis is used to determine whether a livestock business is feasible. This follows Elvia (2016), which states that the value of the R/C ratio can be used to determine the condition of a profitable or loss-making business so that it can be determined whether a business is feasible or not. A value analysis of the R/C ratio of broiler farms in Kaliwungu District, Regency Kudus, could be seen in Table 4.

Based on the data in table 4, it is known that the R/C ratio strata I was 1.102, and the R/C ratio strata II was 1.082. The R/C ratio values of strata I and II are greater than II, indicating that the broiler chicken business in Kaliwungu District is profitable and feasible to continue. This is based on Payman’s decision (1993) which states that if the value of the R/C ratio is > 1, the livestock business can be said to be feasible and profitable. This is also supported by the opinion of Rinto et al. (2018), which states that the value of R/C > 1 means that the activities in chicken farming that are carried out can be said to be feasible because the activities provide higher revenue compared to the costs.

| Item | Strata I | Strata II | |

| 1. | Revenue (IDR) | 585,560,902 | 1,556,632,930 |

| 2. | Cost | 531,582,400 | 1,439,024,367 |

| 3. | R/C ratio | 1.102 |

1.082 |

Sources: Primary data 2022

Payback Period (PP) analysis

Table 5 shows that the value of the payback period in strata I was 12.777 periods and 2.555 years. This shows that the return on investment for broiler chicken farming in strata I when farmers raise was 12,777 periods or in 2,555 years. The value of the payback period in strata II is equal to 18.039 periods and 3.609 years. This shows that the return on investment for broiler chicken farming in strata II was 18.039 or over 3,609 years.

Table 5: Payback period Analysis

| Item | Strata I | Strata II | |

| 1. | Investment (IDR) | 689,691,500 |

2,121,382,500 |

| 2. |

Profitability per period (IDR) |

53,978,502

|

117,608,564

|

|

3. |

PP (periods) | 12.777 | 18.039 |

| 4 | PP (year) | 2.555 |

3.608 |

Sources: Primary data 2022

Comparison between period I and II payback period values are faster in strata I. This is because the profitability of strata I was higher than that of strata II. This is because in strata II the investment costs incurred are more significant than in strata I because the equipment and cages in strata II livestock businesses are more sophisticated and more expensive, so it takes longer to pay back the investment. This follows the opinion of Nurisi et al. (2022), which states that if the initial investment value is small with a large net cash flow obtained, the payback period will be faster and vice versa.

Normality Data Test

Testing for normality in this study was carried out by using the non-parametric statistical test of Shapiro – Wilk analysis. The normality test on strata I profitability obtained a significance value of 0.391 > 0.05, so it can be concluded that the residual data is normally distributed. The normality test on strata II profitability obtained a significance value of 0.191 > 0.05, so it can be concluded that the residual data is normally distributed.

One Sample T-test

The percentage value of profitability in broiler chicken farms in Kaliwungu District for each stratum needs to be known whether there is a difference from BRI’s bank deposit interest in October 2021, which is 6.84% using the one-sample t-test. The results of the analysis are presented in Table 6.

Table 6: Compare mean using One Sample T-test

| Result | ||

| Strata I | Strata II | |

| T-test | 2386 | 2029 |

| Asymp. Sig. (2-tailed) | 0.041 | 0.057 |

Sources: Primary data 2022

The sig is known based on the data from the one sample t-test and different test results in Table 6. (2-tailed) strata I of 0.041<0.05, then H0 is rejected, and H1 is accepted. This shows a significant difference between the value of livestock profitability at the strata I level and BRI Bank deposit interest. The value is sig. (2-tailed) strata II of 0.057 > 0.05, then H0 is accepted, and H1 is rejected. This shows that the profitability of livestock at the strata II levels and Bank BRI’s deposit interest are the same. Based on the calculation of the average profitability in strata, I is higher than BRI bank deposit interest, so broiler chicken farming is profitable compared to BRI bank deposit interest.

CONCLUSIONS And RECOMMENDATIONS

The most considerable fixed costs incurred in a production process in strata I and strata II are the depreciation of cages and equipment. Variable costs that are the most expended in a production process in strata I and strata II are found in the purchase of feed which is around 70%. Kaliwungu District, Kudus Regency is profitable, with strata I level more profitable than strata II. At the strata II levels, there is no significant difference between the profitability of livestock and Bank BRI’s deposit interest; at the strata I level, there is a significant difference between the profitability of livestock and Bank BRI’s deposit interest.

Farmers can increase the value of profitability by increasing the value of IP and adjusting the density of chicken; besides that, they can also regulate how to feed them so that they are absorbed more and increase the weight of the chickens optimally, and most importantly, it is more cost-efficient.

ACKNOWLEDGEMENTS

The authors would like to thank the Faculty of Animal and Agricultural Sciences, who funded this research.

CONFLICT OF INTEREST

The authors state that there are no conflicts of interest.

novelty statement

This research seeks to analyze the most profitable broiler chicken business for farmers in Indonesia. A well-managed broiler chicken business will increase the broiler chicken farmer’s income.

AUTHOR’S CONTRIBUTION

All authors contributed to the conduct of the research, the writing process, and the data analysis.

REFERENCES

Elvia R. (2016). Analisis nilai tambah ubi kayu sebagai bahan baku keripik singkong pada home industry Pak Ali di Desa Ujong Tanjung Kecamatan Mereubo Kabupaten Aceh Barat. Skripsi. Aceh:. Universitas Teuku Umar Meulaboh.

Hastuti D., R. Prabowo, dan A.A. Syihabudin. (2018). Tingkat hen day production (hdp) dan break event point (BEP) usaha ayam ras petelur (gallus sp). J. Agribisnis Universitas Malikussaleh. 3(2): 64-72. https://doi.org/10.29103/ag.v3i2.1111

Hayati N., H. M. Ferichani dan I. Khomah. (2019). Analisis usaha ternak ayam broiler di Kabupaten Karanganyar. J. SEPA. 15 (2): 156 – 163. https://doi.org/10.20961/sepa.v15i2.26972

Maulana F. (2017). Dugaan Terjadinya Intergrasi Vertikal dalam Usaha Peternakan Ayam pada UU No. 18 Tahun 2009 Tentang Peternakan dan Kesahatan Hewan. Skripsi. Makassar: Universitas Hasanuddin.

Nurisi N., I. L. S. Munthe, dan R. Y. Sari. (2022). Analisis kelayakan usaha dengan metode (revenue cost ratio, payback period dan net present value) pemakaian alat tangkap nelayan kelong apung di Desa Berakit Kecamatan Teluk Sebong Kabupaten Bintan. Student Online Journal (SOJ) UMRAH-Ekonomi. 3(1) : 177-183.

Paly M. B. (2016). Analisis profitabilitas peternakan broiler pola kemitraan berdasarkan skala kepemilikan di Kecamatan Bontonompo Kabupaten Gowa. J. Ilmu dan Industri Peternakan. 3(1) : 64 -78.

Payman S. (1993). Pengantar Evaluasi Proyek. Gramedia. Jakarta.

Prasetiyo D. B., A.W. Muhaimin dan S. Maulidah. (2018). Analisis nilai tambah nira kelapa pada agroindustri gula merah kelapa (Kasus pada agroindustri gula merah Desa Karangrejo Kecamatan Garum, Blitar). J. Ekonomi Pertanian dan Agribisnis. 2(1): 41-51. https://doi.org/10.21776/ub.jepa.2018.002.01.5

Purbajanti E.D., A. Setiadi, W. Roessali. (2016). Variability and nutritive compounds of guava (Psidium guajava L.). Indian J. Agricult. Res. h 50: 273 - 277. https://doi.org/10.18805/ijare.v0iOF.10280

Rukmini R., M. Mardewi, dan R. Rejeki. (2019). Kualitas kimia daging ayam broiler umur 5 minggu yang dipelihara pada kepadatan kandang yang berbeda. J. Lingkungan dan Pembangunan. 3(1) : 31-37.

Santoso S.I. ,Sarjana, T. A., dan A., Setiadi A. (2018). Income analysis of closed house broiler farm with partnership business model. Bulet. Peternakan, 42(2): 164-169. https://doi.org/10.21059/buletinpeternak.v42i2.33222

Setiadi A., T.A. Sarjana, T. A., S.I. Santoso, dan S. Nurfadillah. (2021), July. Economic analysis comparison between broiler chicken reared in closed house cage and its reared in open house cage. In IOP Conference Series: Earth Environ. Sci .803(1):1-4 https://doi.org/10.1088/1755-1315/803/1/012066

Setiadi A., S. I. Santoso, M. Mukson, W. Roessali. (2022). Contract broiler farming as an effective pathway to improve rural prosperity in Indonesia. Int. Soc. Sci. 1–13. https://doi.org/10.1111/issj.12330

Suasta I. M., I.G. Mahardika, dan I.W. Sudiastra. (2019). Evaluasi produksi ayam broiler yang dipelihara dengan sistem closed house. Majalah Ilmu Peternak. 22(1) : 21-24. https://doi.org/10.24843/MIP.2019.v22.i01.p05

Zentiko B. D., M. Handayani, dan S.I Santoso. (2015). Analisis break even point usaha peternakan ayam broiler di Kecamatan Limbangan Kabupaten Kendal Anim. Agricult. J. 4(1) : 15-24.